Research Article

Research ArticleABSTRACT

This study was conducted from March-July 2021 to assess status and dimension of feed, and livestock product supply, price and marketing constraints and to identify the major factors or reasons contributed to the development of these problems particularly for the past five years. Check list, informant discussions with relevant stakeholders were used to collect suitable data and information. The highest gap of compound feed between supply and demand was recorded for dairy followed by beef and poultry farms. Animal feeds inflation rate (45-55%) was much higher than food inflation rate (24.1%) on the same year from July 2020-July 2021 in Ethiopia. Inflation rate between 2020 and 2021 for egg, milk, beef and chicken meat were 46, 37, 35.5 and 55.8% respectively. From this study, it is possible to conclude that scarcity of feed ingredient and presence of illegal marketing in the value chain were some of the main factors for price increment of compound feed and livestock products.

Keywords: Compound feed; Price; Livestock; Products

Introduction

In developing economies, the livestock sector is evolving in response to rapidly increasing demand for livestock products due to the human population growth, higher prosperity and urbanization [1]. Animal feed and nutrition are the essential link in the livestock production chain that is between crop cultivation and animal protein production and processing. Surging demands and struggling supplies result in stressed surroundings in which animal feed operators and farmers need to balance their activities continuously, taking into account animal performance as well as customer, consumer and societal demands [2]. Earlier study FAO [3] indicated that producing the additional food needed to feed all people and livestock in 2050 will require a 9 percent expansion of arable land, a 14 percent increase in cropping intensity and a 77 percent increase in yields. Ethiopia is a country with largest livestock population in Africa and with a huge livestock genetic diversity.

However, due to various factors, the country is far beyond the utilization of these huge resources. In the second Growth and Transformation Plan (GTP) of 2015, Ethiopian government has identified livestock sector as a new source of economic growth. In order to achieve the GTP plan on livestock sectors, feed subsector is central for all livestock commodities and is a key pillar of livestock growth and transformation from various perspectives. From economic point of view, about 70 percent of the cost of animal production is feed and suggesting economic feasibility of animal agriculture is mainly a function of quantity and quality of nutrients and the science of feeding. Thus feed is a point of convergence and a critical commodity for which all livestock species compete and it is a major pillar towards ensuring economic, social and environmental goals of livestock production [4]. Historically, the development of feed processing plants in Ethiopia dates back to the beginning of modern livestock husbandry in the early 1950’s followed by establishment of feed processing enterprises during the socialist regime. As a follow up of the new economic policy since 1991, the feed processing enterprises operated by government were privatized and a number of feed processing plants of various capacities came into operation [5].

Availability, quality and escalation of price of commercially manufactured feeds have been reported to be a major problem affecting the feed and livestock industries involved and consumers. Commercially manufactured feeds are important input for marketoriented poultry, dairy and beef production system in Ethiopia accounting for about 70-80% of total cost of production. The share of commercial feed in the total supply of all feed sources in the country is increasing from time to time to satisfy the emerging sector of poultry, dairy and beef enterprises. From [6], data on supply, demand and price over the last five years indicates that there has been a steady increase of demand, price and supply shortage of this commercially processed feeds. This situation is feared to reach a crisis proportion unless there is an emergent response to this very important demand and supply gaps that lead to high price. This issue needs attention of policy makers, development agencies and the private sector concerned to draft short- and long-term intervention plans to minimize the effects on the general economy, consumers and private sector to survive in the face of this harsh marketing realities.

Statement of the Problem

In the recent years supply and price situation of feeds and feed ingredients have shown a steady decrease and increase respectively but the dimension of this general trend was highly aggravated in the last one or two years probably due to current development related to the general inflation of food commodities in the country negatively affecting the feed and animal production sub-sector as well [4]. Commercial feed processors and modern poultry, dairy and beef farms which are seriously confronted by this supply and escalation of price are voicing their concern requesting the responsible government bodies to intervene to solve this issue through forming positive environment that encourages both private sectors involved in feed manufacturing and modern animal production.Therefore the ministry of trade and industry precedes initiative to handle the issue and establish study team from different institutions to assess the cause of the problems mentioned above and propose policy recommendation.

Scope of the study

The scope of the study is focused on commercial feed processors, price and marketing situations in market-oriented poultry, dairy and beef farms. Hence, this study was initiated with the following objectives:

General Objectives

Assessing the current compound feed and livestock product supply, price and market related constraints.

Specific objectives of the study are:

a) Studying the current status and dimension of compound feed demand, supply, price and marketing constraints

b) Indicating the major factors or reasons contributed to the development compound feed related problems particularly for the past five years

c) Identify possible strategic directions for the commercial feed sub-sector and livestock product processing industries

Methodology

The study was undertaken from March-July 2021. In this study data were collected from different private and farmers Union animal feed processors, suppliers, flour and oil industries, associations. Besides, data were collected from livestock farms like poultry, dairy, beef and others.

The methodology employed during the course of the study is indicated as follows:

a) Basic information was collected by using check list

b) Informant discussions were used to understand details of particular issues regarding key challenges and strategic directions of feed processing plants

c) Desk reviews were made from print media including published and unpublished materials, websites and others

Data Source

Primary and secondary data were collected from feed processors, poultry, dairy and beef farms, Government organizations, different associations, previous studies, different reports, prospective plans.

Data Type Used for the Study

Data were collected on production, consumption, market supply of compound feed of the year 2016/17-2020. Compound feed price, livestock product price data for the past five years were collected. Current data on direct employees at on farm, feed industry and livestock product processing industries were included.

Statistical Analysis

A Generalized linear model (Proc GLM) procedure of SAS (SAS, 2008) was used for the analysis of cereals and oil crops production and utilization from 2016-2020. The effects of year and crop type were included in the model. Then the analyzed data were organized using descriptive and inferential statistics. When there was significant difference of dependent variables among independent variables mean, comparison was undertaken using Tukey-test at P value of 95%. The model was:

Result and Discussion

Feed Ingredients Demand and Supply Dynamics

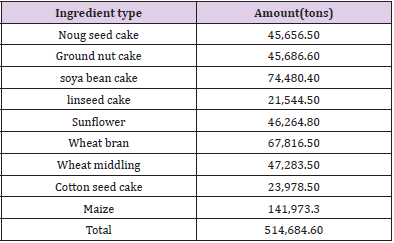

The major ingredients used to formulate compound feed include maize, sorghum, flour processing by-products (wheat bran, wheat short, rice bran), different kind of oil seed cakes (soyabean meal, Nuog seed cake, linseed cake, groundnut cake, cotton seed cake, sesame seed cake, and others), molasses, and ingredients that are added in tiny quantities to boost production (vitamins, minerals, amino acids and premixes). A list of the ingredients demanded by feed industry in 2020/21 is presented in (Table 1). As indicated the highest amount of ingredient required by feed industries is wheat followed by maize and soyabean. This is because compound feed for ruminant required more volume of maize and wheat by products (wheat bran and wheat middling) and soyabean is mainly required for poultry. Generally, demands for feed ingredients by feed processing industries were increased from 120,897 to 574,734 tons between the study periods. However, the supply of feed ingredients for feed industries was only around 50% (Table 2) and (Figure1).

Table 1: Feed processing ingredient quantity demand by types in 2020/2021 EC.

Note: Source: Calculated from design capacity of feed companies.

Table 2: Total feed ingredient demand, supplied and deficit quantity.

Note: Source: calculated from the Feed company design capacity.

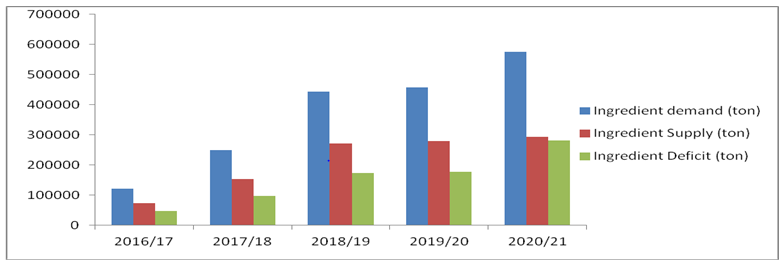

Figure 1: Total feed ingredient demand, supply and deficit.

As Figure 2 shows demand of feed industries was increased at a faster rate than supply in the study periods. With this deficit, the feed industries had performed below their capacity. The deficit in feed industries is related with low market supply of wheat for flour industries to produce wheat bran and wheat middling, absence of the produced maize for the industries and the lower local market supply of oil seeds. This shows that as livestock sectors intensifies protein meal and cereal use would expand. This expansion should be supported by increasing oil seeds and cereal production and supply to the market. However, as observed in Table 1 market supply (sale to the market) for oil seeds and cereals were lower than the demand. The study [3], indicated that as livestock production intensifies in the coming years, protein meal use expands across most of SSA, with the fastest growth recorded in Western Africa (43%) and Eastern Africa (32%). This implies that the demand for oil seed and oil seed cake would be increased and it could be a good opportunity to produce more oil seed to utilize locally and to export.

Figure 2: Animal feed price increment index.

The production of cereal grain crops in Ethiopia is destined for human consumption. Consequently, only the milling by-products such as maize bran and wheat bran are available for livestock feed production. Maize bran and wheat bran are the most commonly used cereals. The most widely available oilseed cakes are Noug and sunflower. All the feed premixes are imported. The raw materials available to the animal feed industry are generally those that are produced within the country. These include oilseeds (soya, cotton and sunflower seeds maize, maize bran, wheat bran, soya cake and cotton cake.). The livestock industry is a driving demand for animal feeds especially for poultry, and poultry feed accounts over 60- 96% of the compound feed. The high demand for poultry feed is driven by increasing demand for poultry products especially due to population increase that is becoming urbanized, and higher levels of disposable income.

The highest demand for livestock products would appear that growth in the animal feeds industry will be driven by growing demand for livestock products. However, this growth has been slow owing to limited production of the major ingredients. The projected increase in demand for animal feed will put pressure on the availability of raw materials. It follows then that to meet this demand, there needs to be a corresponding increase in production of raw materials such as maize, wheat and oil seeds and as a result their by-products would be available for feed processing industries.

Compound Feed Demand by Species

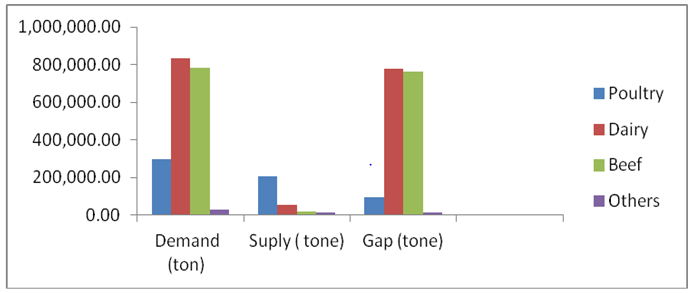

The demand for animal feed is a function of livestock population, price of feed, price of substitutes, and other exogenous factors. From the data generated in 2020/21 from 60 (sixty) feed industries found throughout the country dairy, beef and poultry demanded higher volume of compound feed in their order of importance (Tables 3 & 4 and Figure 3). However, only 6.3, 2.6 and 68.7% of the compound feed were supplied for dairy, beef and poultry farms respectively. The highest gap between supply and demand was recorded for dairy feed followed by beef and poultry farms. The higher gap for ruminant is due to scarcity of wheat and non-appearance of maize in the market. Generally, the gap in supply and demand implies scarcity of cereals and oil seeds in the market, inaccessibility of some cereal (maize) in the market and as a result rising of prices and affordability of compound feed to the livestock farms. From production point of view, animal production is essentially a conversion of feed into animal product which dictates the level of production and product quality and safety. From economic point of view about 70 percent of the cost of animal production is feed and suggesting economic feasibility of animal agriculture is mainly a function of feed. The demand for animal feeds is derived from the demand for animal source food. The general trend in this regards is that demand rises in animal source food is in response to urbanization, increasing in population (3%) annually, increases in income at disposal, GDP growing at 7-8%, and preferences to ASF [7].

Figure 3: Total feed ingredient demand, supplied and deficit quantity for the year 2020/2021.

Table 3: Feed demand and supply for the years 2020/21.

Note: Source: Calculated from number of animals need this feed.

Table 4: Employment created by feed industries and commercial farms.

These demands justify the demand for compound feed is associated with intensification of livestock production to meet the growing demand. The demand for livestock commodities in Ethiopia is rapidly growing. Compared to the production base year of 2014/15 with estimated 167million liters of milk, 1.3 million tons of red meat and 419 million eggs, the projected demand is expected to be 1490 million liters of milk, 1.9 million tons of red meat and 3.9 billion eggs by 2020 [3]. There is a policy push to improve the current per capita consumption of livestock products in Ethiopia. However, currently one of the lowest in the World (9 kg meat, 56.2 liters milk, 4 eggs; [3] which is urgently calling for production increment and productivity improvement. Projected increment in the demand and production of beef, poultry, and others lead to substantially higher demand for compound feed. Under the baseline, the combined demand for cereals and oilseeds used as livestock feeds increases from 304,300 MT in 2010 to 608,900 MT in 2030 and 1,085,100 MT in 2050.

For this increment population growth, urbanization and income growth are important factors. These projections of feed demand quantities reflect impacts of both future economic and climatic change and are more variable in 2050 than in 2030. (FAO, 2019).

Feed and Feed Ingredient Price

Compound feeds are the sole diet for semi-intensive and intensive poultry and commonly used by dairy and fattening farms. The supply of these feed ingredients is challenged by low production of feed ingredients, rising prices and quality. Consequently, affect the access and affordability of processed feeds to livestock producers. Feed prices are determined mainly by the supply of feed, the number of animal units to be fed, and the level of livestock product prices. In recent years there are several reports from feed processors, policy makers and farmers on the rise of feed price. According to producers’ associations this situation is leading to the closing of some commercial farms both dairy and beef producers, due to low return on investment. This is supported by Joe (2008) stated that when grain prices spike can be more production of red meat and poultry, as herd sizes are reduced and/or as more animals and milk are sold to maintain cash flow to cover higher prices. This can depress farm (and wholesale) prices at least temporarily, further exacerbating the cost-price squeeze.

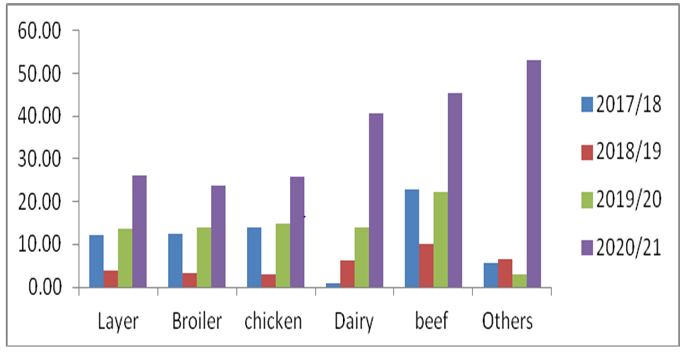

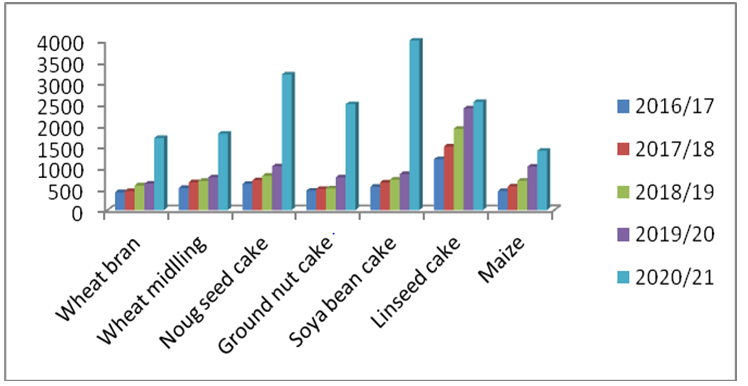

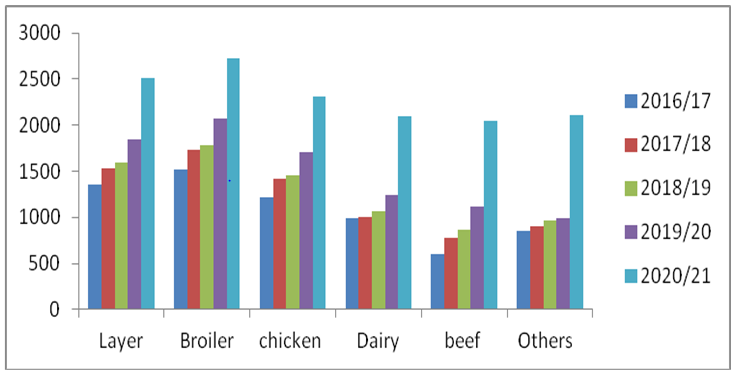

If current market conditions persist, meat supplies will decline and prices rise through producer attrition and reduced capacity. According to Figure 3, price of feed ingredient has shown continues increment over the past five years from 2016/17 to 2020/21. Comparing the increment growth between the base year 2016/17 and 2020/21 has shown 303.8, 244, 416, 443.5, 627.3, 112.5 and 211% for wheat bran, wheat middling, noug, groundnut, soya, linseed cake and maize respectively. The highest price increment was observed in soya bean followed by ground nut and noug seed cake. Similarly, compound feed price for different species was increased by 85.5,80, 89.6, 110.8, 239.4 and 148.8% for layer, broiler, chicken, dairy, beef and others respectively (Figure 4). The highest average price growth rate of compound feed for five years was observed in beef and dairy farms which are negatively related with the highest gap for demand and supply of compound feed for dairy and beef farms.

Figure 4: Feed ingredients price (9ETB/quintals).

Figure 5: Animal feed price (ETB/quintals).

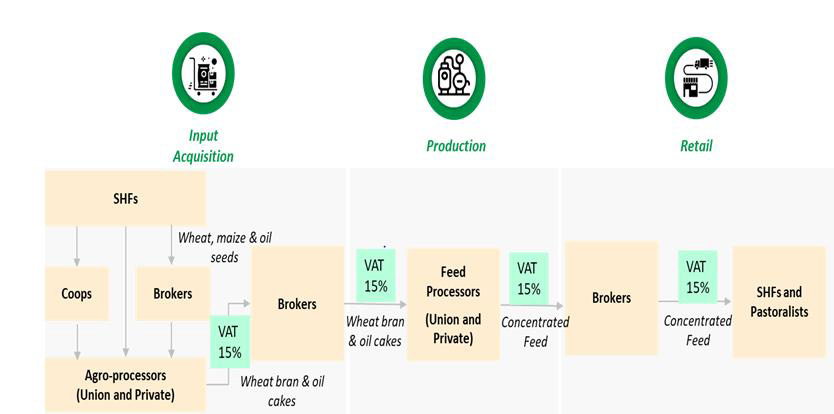

This implies that feed supply and feed prices are negatively correlated. The lower production of cereals and oil seeds in 2019 production years have brought the maximum inflation rate in 2020 on different feed ingredients and compound feed of different species. This price surge of animal feed is induced by significant rises in the price of feed ingredients due to supply shortage and other factors. From the point of view of the supply of compound feeds, the principal cost is that of raw materials, which amount as much as 80% of operating costs and additionally there is high transport costs. According to a study by MOA and ATA 2021 the other reasons for the high prices of feed ingredients and feeds are VAT and other taxes imposed on the feed ingredients. Multiple taxations due to unnecessary long supply chain could add the VAT imposed on feed ingredients up to 60% or more (Figure 5). The involvements of brokers along the marketing chain lead to multiple taxation and elevate the price of ingredients and compound feed.

Animal Feed Ingredients and Compound Feed Inflation Rate (Price Index) for Different Species

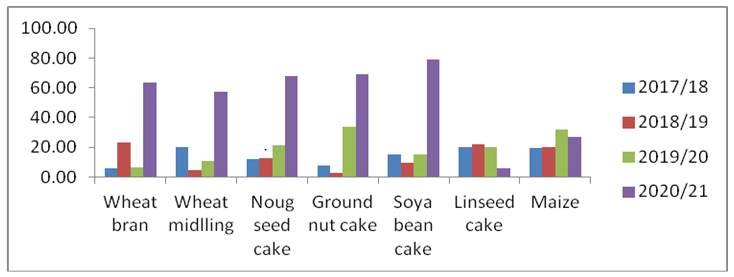

As observed in Figure 6 the highest inflation rate (price index) for compound feed was observed in the year 2020/2021 as compared with the previous year on shoat farms followed by beef and dairy farms with the value of 55, 48 and 45% respectively. Lower price index with one digit was observed in 2017/18 production year which result from high production of oil seeds and cereals in the previous year. With regard to feed ingredients of soya bean, inflation rate (price index) was higher (>50%) than all in 2020/21 followed by ground nut, noug cake and wheat products (Figure 7). As [6-10] indicated, the country level food inflation rate was 24.1 percent in July 2021 as compared to the previous year. This shows the animal feeds inflation rate (45-55%) was much higher than food inflation rate on the same year in Ethiopia. This implies the abnormal inflation of animal feed which may be due to less production and scarcity in the market of oil seed and cereals. In addition there are many factors including illegal marketing in long value chain and artificial/ manmade.

Figure 6: Feed ingredient price increment index.

Figure 7: Average animal product price.

Price Increment Trend of Animal Source Food

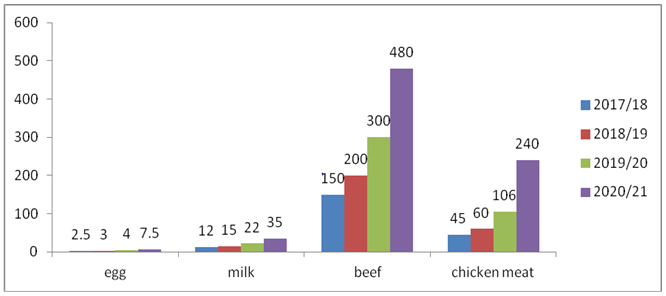

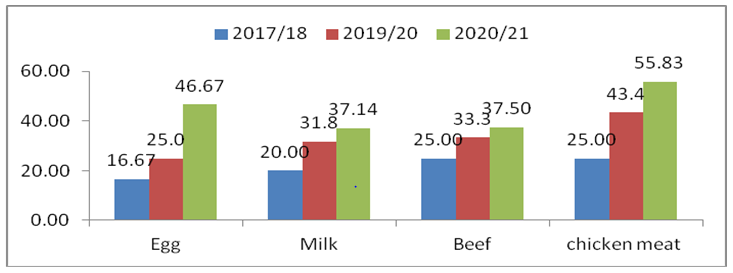

As Figure 8 indicate the price of milk, beef, egg and poultry meat has raised at least three folds in the past four years with highest increment in 2020. Feed is the largest single cost item for livestock production, accounting for 70%– 80% of the total cost although energy, labor, and other inputs have increased in the last 5 years. As Figure 9 indicated, inflation rate between 2020 and 2021 for egg, milk, beef and chicken meat were 46, 37, 35.5 and 55.8% respectively. As price takers in competitive markets, animal producers cannot simply pass their higher costs on to consumers. To date, rising costs have largely been absorbed by livestock and poultry producers, often with significant financial loss. However, higher costs of production will ultimately reflected in higher prices for meat, milk, and eggs at retail counters. This apparently reduces the affordability of livestock products by consumers and will reduce purchasing power of consumers.

Figure 8: Animal product price increment index (%).

Figure 9: Industry product is plagued by inefficient linkage between actors leading to decrease production quantity, multiple taxes and higher price.

This in turn reduces the demand of livestock product by the consumers and livestock producers reduce their supply and would go to bankruptcy or financial loss. This will also affect the current per capita consumption of livestock products in Ethiopia, which is one of the lowest in the World (9 kg meat, 56.2 liters milk, 4 eggs; [3]. In contrary to the current higher inflation rate on beef meat in Ethiopia which would reduce beef consumption and production, the study [2] described that beef consumption growth is strong across the region (SSA), expanding by 2.6% to 2025. Growth is particularly strong in Eastern and Western Africa, where rates exceed 4%. Within these regions, consumption growth is mainly driven by Kenya, Tanzania, Ethiopia, Zambia and Nigeria, all of which increase consumption by an annual average of at least 3%. The same study continued that notwithstanding the small base, the projected expansion of 35% in total meat consumption by 2025 outpaces any other region in the world.

Underpinned by rising incomes, urbanization and sustained population growth, robust consumption growth is projected across most of SSA, with an expansion of more than 38% evident in Central, Western and Eastern Africa. Egg consumption provides an important alternative that reflects consumption growth of 36% over the ten year period. Consumption growth is also robust across the region and exceeds 50% in Eastern Africa. This all shows the high demand of animal products in Africa which provide high local and export market for Ethiopia. Livestock improve food and nutrition security as ASF are rich in major and micro-nutrients. ASF are a major source of iron, zinc, calcium, riboflavin, vitamin A, vitamin B-12, and retinol, which have numerous benefits including linear growth, cognitive development and general health, leading to long term improvements in income and productivity.

Milk in particular contains several critical micronutrients such as calcium, vitamin A, riboflavin and vitamin B12 that are essential for growth and development of children older than 12 months. Children, pregnant and lactating mothers should be receiving ASF, whose consumption currently is quite low. However, to assure that this increased local demand can be met by local supply and not by imports, more attention will need to be paid to feed price and the facilitation of an enabling environment that will allow for efficient livestock feed industry.

The Status of Compound Feed Industry

Over the past decade, the use of compound feed and feed supplements has increased. In the year 2020/21the livestock feed industry required 1,944,490tons of compound feed. Unfortunately, despite adequate installed production capacity, only 292,761.90tons of feed were produced. The shortfall in production was attributed to an inadequate supply of raw materials. A total of about 32 privately owned and 28 cooperatives feed processing plants are currently operational in Ethiopia. The feed processing plants owned by private companies and cooperatives engaged in production of compound feed. In terms of facilities, all the privately owned feed processing plants have feed mill, mixer and storage places for ingredients and for processed feeds. Only few plants mill limestone and make multi-nutrient blocks.

Pellet maker is limited to two feed processing plants, liquid mixer exists only in one feed processing plant and no feed processing plant has a laboratory for analysis of ingredients and feeds. Most feed processing plants are currently operating below their installed capacity mainly due to low demand for the product, shortage of ingredients supply and inconsistent supply of electricity. Average operational capacity of feed processing plants at farmers’ unions level is 2.0 tones per hour [5]. In terms of operational capacity as percentage of installed capacity for the feed mixer, farmers’ unions are currently operating at an average processing capacity of 66 percent. Traditionally the feed industry has been linked to the supply of the raw materials, as these were generally the by-products of other processes and of low value relative to the main product. However, market orientation mainly as a result of advances in nutritional science the value has improved to great degree. At the same time nutritional knowledge has become more widespread, so that the demand for byproducts has increased and their prices have risen, thereby reducing the advantages of supply orientation. At the same time, since the distribution system is often poor, and since feeds are usually made for particular markets, sales advantages are likely to be gained from market proximity.

Employment and Socio-Economic Importance

The feed manufacturing industry also plays an important role in the socio-economic development in the country, making important contributions to employment, income generation, and to linkages within the value chain. Furthermore, an efficient animal feed industry, producing affordable feed of high quality, can help and ensure that smallholder livestock keepers are not excluded from the market opportunities presented by the socio-economic transformation taking place.

Marketing of Compund Feed

Even though Agro-industrial factories (flour mills, oil mills) are VAT registered, they sell their products to middlemen, and the brokers without a receipt. This make that the market is engulfed in illegal trade and leading to widespread shortages and inflation. On the other hand, the lack of market linkages and the lack of chain of command have created favorable conditions for brokers and traders. Several government institutions are actors in supporting the feed industry development; however, there are weak interests to collaborate and coordination efforts. It is common practice of making decisions on feed industries without taking situation of the food processing industries into account. The lack of a formal marketing system for the by-products of the flour and oil mills used by the feed industry and the lack of a single institution around the market is creating a serious problem for the feed and fodder inputs and creating favorable conditions for brokers and greedy traders to lower their prices.

Conclusion

The highest gap between demand and supply was recorded for dairy compound feed followed by beef and poultry. Inflation rate of feed ingredients and livestock products (the product of feed ingredients) were higher as compared to inflation rate of food items. Feed prices are determined mainly by the supply of feed, the number of animal units to be fed, and the level of livestock product prices. Main reasons for the high prices of feed ingredients and processed feeds are VAT and other taxes imposed on the feed ingredients, export of feed ingredients, oil seeds and oil factory by products. Multiple taxes due to unnecessary long supply chain adds the VAT imposed on feed ingredients up to 60% or more.

Acknowledgment

I would like to express my sincere gratitude and heartfelt thanks to Ethiopian Meat and Dairy Industry Development Institute management for supporting me financially. I sincerely acknowledge the help and co-operation rendered for the animal feed processing industries and other organizations as a whole.

References

- Seyoum Bediye, Gemechu Nemi, Harinder Makkar (2018) Ethiopian feed industry: current status, challenges and opportunities. Animal feed resources information system.

- Den Hartog LA, Sijtsma R (2012) Innovation in animal feeding, a key driver in the concept of sustainable precision livestock farming.

- (2019) FAO. The future of livestock in Ethiopia. Opportunities and challenges in the face of uncertainty. Rome, p. 48.

- (2021) Harinder 2018 Report on feed inventory and feed balance in Ethiopia: FAO 2018 Grain and Feed Annual report 2021.

- Makkar HPS (2016) Animal nutrition in a 360-degree view and a framework for future R&D work: towards sustainable livestock production. Animal Production Science 56: 1561-1568.

- (2021) CSA. Agricultural productivity and inflation.

- ILRI (2019) Options for the livestock sector in developing and emerging economies to 2030 and beyond. Meat: The Future Series. Geneva, Switzerland: World Economic Forum.

- Hartog, R Sijtsma (2012) 6d Annual meeting of the European.

- Thornton PK (2010) Review Livestock Production: Recent Trends, Future Prospects. Philosophical Transactions of the Royal Society B: Biological Sciences 365: 2853-2867.

- Philip K Thornton (2010) Livestock production: recent trends, future prospects. Biological sciences 365: 1554.